The Stablecoin Landscape

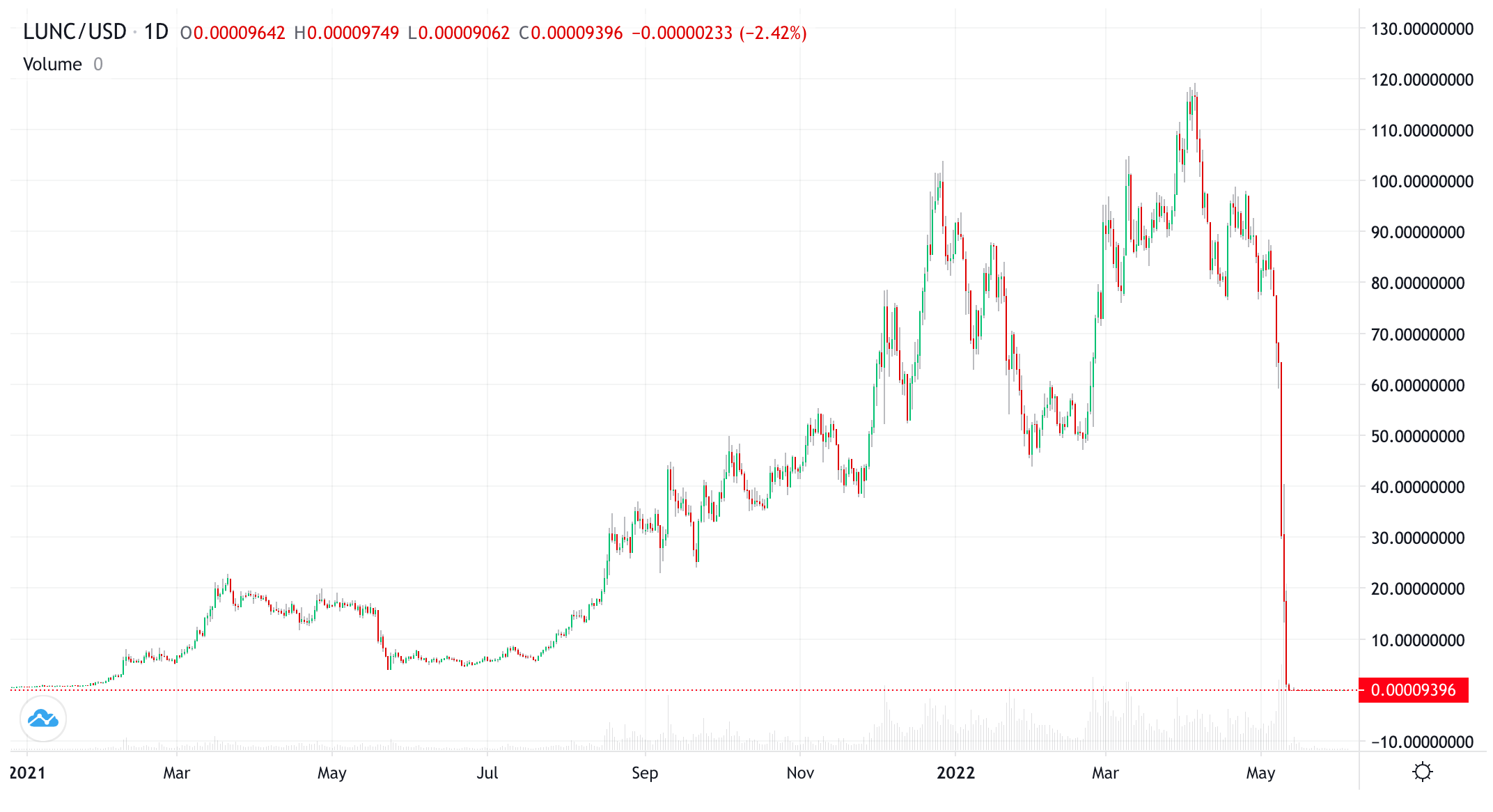

The landscape for algorithmic stablecoins has shifted since the collapse of Terra. The Terra ecosystem, worth over $60 billion at its peak, is now all but dead. Whether it can be resurrected remains to be seen. The collapse took nearly all of the trust accrued towards seignorage algorithmic stablecoins. But Terra also taught us lessons that we can take forward and use to evaluate both current and emerging stablecoin protocols to ensure that history doesn’t repeat itself.

Terra operated with the logic of a 2010s Silicon Valley startup. It had a founder with a big ego, it was willing to light cash on fire in the name of growth, and it was weighed down by overengineering and complexity. Ultimately, UST and its partner in crime, LUNC (née LUNA), came to a steep end.

The brash, ego-driven leadership style that drove Terra to dizzying heights should have been the first red flag. This leadership style burns the bridges and the boats (and $60 billion) and ends poorly when the hype and bravado start to wane. In the end, the whole thing collapses under the weight of all the smoldering resentment and scorched trust. It turns out those bridges and boats served a purpose after all.

We’ve heard this story before. It’s the tale of Travis Kalanick and Uber’s tailspin and the implosion of WeWork and its generously-egoed founder, Adam Neumann. At some point, we’ll have to learn that business fundamentals matter and that salesmanship and hype are not enough to sustain a massive corporation or billion-dollar financial product. The economic sugar rush always leads to a crash.

But through all the carnage, the stablecoin remains a valuable and innovative financial product. If we want stables1 to survive and prosper, we must turn to the incumbents with the lessons learned from Terra to derive a framework for what works and what does not.

To Be Stable in an Unstable World

Stablecoins exist to address the volatility of cryptocurrencies.

Aside from price stability, stables make it easy to transfer value across blockchains. While most commonly pegged to the US Dollar, stables can reflect the price of any currency or asset, including other fiat currencies or other physical assets like gold.

In large part, stables are issued into circulation by an entity that receives collateral in exchange for newly minted (read: created) tokens. These tokens can then be exchanged on the open market. Finally, the issuing entity offers redemptions for circulating tokens in exchange for the underlying collateral. This mechanism is how Tether works, but not how Terra worked.

Terra is a seignorage-style algorithmic stablecoin that is only partially collateralized. For an eerily-foreshadowing look at the thinking of Terra’s founder Do Kwon, see his article from 2018 explaining his theory for scaling seignorage. Bolding is mine, italicization is Kwon’s.

“The most popular flavor of stable-coins these days are those that are 100% fiat collateralized, such as Tether, Circle, Gemini and Paxos. Several decentralized stable-coin projects such as MakerDao go even further, and maintain well over 100% reserves in cryptocurrencies. Though this is a responsible approach in designing fault tolerant systems, I think it’s also equally uninspiring; such systems make zero assumptions about the demand floor for their currencies because they were not designed with serious consideration of go-to-market strategies to capture long-term demand. Here we can do better. If we could somehow drive deterministic demand for the stable-coin, we could lower the cost of collateral and capture value by printing money.”

It turns out you can also destroy value by printing money. Here, Kwon describes an under-collateralized stablecoin supported by marketing spending and hype. This also foreshadows Kwon’s plan to offer 20% APY on Terra’s lending platform Anchor (which was advertised as a savings product—I suspect this will be a hot topic of discussion in the coming hearings and regulation). The 20% APY was essentially a marketing expense for the Luna Foundation Gaurd (LFG). Clearly, 20% APY is not sustainable. The idea was to use the attractive APY to front-load demand into the system and decrease the APY over time as UST gained adoption.

This leads us to our framework for evaluating stablecoins. Below is the Stablecoin Trilemma, laid out by Multicoin Capital:

The Stablecoin Trilemma remains a good starting point for a stablecoin evaluation framework. I would add that under-collateralization poses an equal risk to long-term stability as capital inefficiency. Untested algorithmic mechanisms also pose significant risks at scale (as we have seen). The complexity required in maintaining price stability without the easy-to-understand collateral mechanism has posed significant risks to investors.

I propose the following framework that adds “Easy to Understand” as a fundamental criterion. Risk hides in complexity.

Price Stable

Capital Efficient

Easy to Understand

Decentralized

This framework serves as a guidepost for investors to evaluate stablecoins before allocating capital to a stablecoin product.

Now, let’s figure out which stablecoins deserve the focus of our analysis.

Isolating the Major Stables Within the Crypto Market

While Bitcoin remains the dominant coin with a market cap of $565 billion2, followed by Ethereum with a market cap of $214 billion, the third-largest cryptocurrency is Tether—a fully-backed stablecoin with a current market cap of $73 billion. Let’s take the top ten coins and compare the sum of their market caps to the total crypto market cap.

According to listings on Nomics, there are 13,984 cryptocurrencies in circulation. Referencing the breakdown above, we can see that 81.4% of the entire crypto market cap is concentrated within the top ten coins. The remaining 18.6% of value by market cap is relegated to the other 13,974.

Given the steep concentration of value towards the most well-known currencies, we will disregard the long tail in favor of the top ten. Among the top ten coins, three are stablecoins. These are Tether (#3 overall by mkt cap), USD Coin (USDC), and Binance USD (BUSD).

Let’s start by focusing on Tether.

Tether (USDT)

Arguably the best-known stablecoin on the market, Tether is fully backed by a reserve comprised of cash & cash equivalents, bonds, loans, and crypto. Tether can be redeemed 1:1 for fiat via Tether’s redemption portal. The breakdown of Tether’s audited reserves is below:

In addition to its stablecoin offering, Tether also offers exposure to gold via its XAUt token. Each token represents ownership of one fine troy ounce of gold on a specific gold bar. XAUt holders can match their holdings to specific gold bars via a serial number. Holders also have access to purity metrics and weight which can be accessed via a look-up site. Currently, the minimum investment is 50 XAUt, which is equivalent to 50 fine troy ounces, or about $90,000 as of January ’22. XAUt can also be acquired on the open market in fractions as small as the exchanges allow.

Tether’s Strengths

Trust and Stability. Tether is fully-backed, so investors can trust that Tether’s system is fully collateralized by an actively managed basket of reserve assets. Bank runs are less of a risk here.

Brand Name and Wide Adoption. Tether is well-known. This recognition leads to the potential for widespread adoption. Especially when institutional adoption is the marker for the arrival of crypto as a fully-fledged asset class. In this light, JP Morgan has upgraded crypto to its preferred alternative asset.

Tether’s Weaknesses

Tether is centralized. Decentralization is a big part of the Stablecoin Trilemma. Tether is not decentralized. There is a single entity that manages the reserves and thus entirely controls the fate of the stablecoin and relies on the trust of its investors. Remember, the premise of a global 24/7 financial system is that it’s supposed to be trustless. This may be fine in the short-term, but in the long-term, this makes Tether effectively a bank on the blockchain—which entails all of the risks that come with the old banking world.

Reporting is quarterly. Ideally, investors would be able to monitor Tether’s reserves in real time. Or at least monthly, as is the case with USDC. The quarterly delay in reporting does introduce some risk, as any material change in Tether’s reserves could take up to three months to be reported to investors.

USD Coin (USDC)

USDC is second to Tether, with a market cap of $54.2 billion. It also enjoys wide name recognition. Like Tether, USDC’s reserves are independently audited by Grant Thornton and posted monthly.

USDC holders have the option to invest in Circle Yield, a fixed-rate, variable-term yield program that is overcollateralized with bitcoin. In keeping with recent DeFi market teachings, we have learned to ask…

“Where does the yield come from?”

The yield in Circle Yield’s fixed-rate investment comes from Circle’s lending partners. Circle lends your USDC to investment partners, who lend it out to the crypto capital markets. A portion of the interest they receive is sent back to Circle, which returns a portion of that interest to you. Currently, Circle Yield’s shortest term of one month offers a 4% fixed rate. Its longest term, 12 months, offers 4.75%.

In addition, Circle’s reserves are independently audited by Grant Thornton. Below is a USDC’s most recent attestation.

USDC Strengths

Trust and Stability. Similar to USDT, USDC is also fully backed by a basket of reserve assets that fully collateralize all circulating USDC on the market. This provides trust and stability to the market and prevents panic-driven bank runs à la Terra.

Name recognition. Unlike other stables in the market, USDC plays directly to the name association people already have with the US Dollar—for better or worse. For many, this familiarity will ease the transition to global, non-government digital currencies—starting with USDC and moving on to less and less skeuomorphic coins. It’s a non-trivial reality that people like things that sound familiar. USDC has that familiar sound.

Volume at scale. USDC has transferred $4.20 trillion on-chain since it was introduced in 2018. It currently has 730K unique holders. The largest stables that achieve real institutional adoption will need to handle the volume that comes with the global financial system putting its weight on these coins. USDC has proven it can handle volume at an institutional scale.

USDC Weaknesses

Centralized. As you are beginning to see, USDT and USDC are similar in their strengths and weaknesses. They both have similar market caps, both are fully backed, both are liquid and widely traded across chains, and both are centralized. The ideal future that crypto is driving towards is global, non-government, trustless, and decentralized. As we have seen, we may have to prioritize those traits as the technology is built and adopted at scale. Both USDT and USDC are global and non-government (aside from the USDC’s name association). However, they are centralized and require some degree of trust, even though independent third-party audits mitigate this.

Delayed Reporting. USDC releases third-party auditing of its reserves monthly, which is more frequent than USDT but still slower than ideal. In a perfect system, reporting would be in real-time so that investors could precisely see how the reserves were allocated at the time of investment.

Binance USD (BUSD)

BUSD is similar to both USDC and USDT in that it is fully backed. The stable is also independently audited—in this case, by Paxos. Third-party auditing is becoming the industry standard for stablecoins at scale.

BUSD Strengths

Regulated by NYDFS via Paxos. This is either a strength or a weakness, depending on your perspective. Either way, it does provide an aspect of trust to investors, and we have established that although the ideals of crypto point to a trustless future—we still need some element of trust to ensure investor confidence.

Integration with a major exchange. Currently, Binance is one of the largest crypto exchanges in the world. For power users (and even casual users) of the exchange, having a native stablecoin within the ecosystem offers significant convenience in transferring value.

BUSD Weaknesses

Better alternatives. BUSD suffers from being third-place to both USDT and USDC, both of which offer similar exposure to a peg of the US Dollar. Perhaps this is not an issue for those deeply embedded in the Binance ecosystem, but for those with no allegiance to any specific exchange, USDT and USDC may be better options for investment.

Regulated by NYDFS via Paxos. This is listed twice on purpose. Regulation by the antiquated, slow-moving regulatory regime in New York is as much a liability as a strength in investor confidence. NYS recently passed a 2-year moratorium on bitcoin mining, signaling that our great state is doing everything possible to limit innovation and write itself out of the future of money. We’ll see how that plays out. Hopefully, saner heads prevail.

Moving Forward

Currently, there are three solid stablecoin options to choose from for investors looking to manage free cash, and those looking for an easy, price-stable way to transact and move value across chains. All three leading stablecoin options are fully backed by audited reserves, and are verified by third-parties to ensure the reserves exist as reported. Although this does not make these protocols decentralized, it does ensure some amount of trust in the short terms. In the aftermath of the Terra collapse, the crypto markets will have to regain investor trust, and this may be the best path to do so. Decentralization will come in time as the technology evolves, and bad actors are purged from the ecosystem. For now, we will have to tolerate imperfect systems, and build upon what we have to move the space forward in a better way.

Sources

Tether: March ‘22 Reserve Audit by MHA Cayman [PDF]

Source: https://assets.ctfassets.net/vyse88cgwfbl/1np5dpcwuHrWJ4AgUgI3Vn/e0dac722de3cea07766e05c52773748b/Tether_Assurance_Consolidated_Reserves_Report_2022-03-31__3_.pdfThe Stablecoin Trilemma, Multicoin Capital

Source: https://multicoin.capital/2021/09/02/solving-the-stablecoin-trilemma/GSR, Chart of the Week: Solving the Stablecoin Trilemma with Algorithmic Stablecoins

Source: https://www.gsr.io/insights/chart-of-the-week-solving-the-stablecoin-trilemma-with-algorithmic-stablecoins/A Note on Cryptocurrency Stabilisation: Seigniorage Shares—Robert Sams [PDF]

Source: https://blog.bitmex.com/wp-content/uploads/2018/06/A-Note-on-Cryptocurrency-Stabilisation-Seigniorage-Shares.pdfUSDC Attestation, Grant Thornton, Apr. ‘22 [PDF]

Source: https://www.centre.io/hubfs/PDF/2022%20Circle%20Examination%20Report%20April%202022.pdf?hsLang=enBUSD Attestations, Paxos [PDF]

Source: https://paxos.com/attestations/

Stablecoins and stables are used interchangeably. The meaning is the same.

All prices and market cap calculations are as of final editing on June 4th, 2022.